Advising Clients since 1980

Behind the Numbers

Below is a table which compares the investment performance of Shoreline Wealth & Investment Management (SWIM) using commingled accounts in our three tactical asset allocation models with that of the S&P 500 and NASDAQ Indexes since 1998. As you can tell, SWIM has performed well against both averages on an average per year rate of return. The S&P 500 is the index SWIM attempts to outperform. SWIM shows the returns of the NASDAQ Index for illustrative purposes but considers this index much too volatile (risky) and not one SWIM attempts to consistently beat.

Investment Performance Assumptions

The table below shows the per year rate of returns for the SWIM, S&P 500 and NASDAQ Indexes in the column under each year listed. The average annual return column is highlighted in yellow for comparison purposes. The average annual return column assumes all money was invested for the entire time period listed. The value column assumes the value of a $1,000,000 investment made on 31 December 1998 and that no withdrawals were taken during the entire time period listed.

Commingled Managed Investment Portfolios

Investment accounts with a liquid net worth less than $1,000,000 can be still be professionally managed for individuals. Commingled accounts are those in which individuals’ money is commingled using investments including mutual funds or variable annuities. This option provides individuals with an opportunity to have their assets professionally managed and broadly diversified at a reasonable cost. Diversified investment advisors fit perfectly into this management strategy. Additionally, each investor in a commingled account receives a separate statement monthly or quarterly, confirmations of each trade, direct access to the portfolio and potential tax savings from employing buy and sell strategies to minimize long and short-term tax consequences.

Three Portfolio Choices

Select from our Conservative, Moderate and Aggressive strategic asset allocation portfolios. Our clients have different investment goals, experience, time horizons and risk tolerance levels. In fact, a single client may have different goals for different accounts including those for personal investments, retirement income, educational or philanthropic funding and so on. Our diversified investment advisors work with our clients to assist in selecting the appropriate portfolio(s) which offer flexibility, and also to select different portfolios as investor needs or goals change.

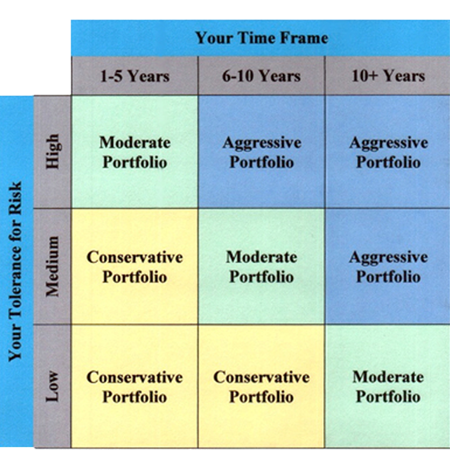

Time Frame & Tolerance for Risk Factors

We have different weightings in different markets and market sectors for each of our three portfolios which we offer and re-balance these portfolios regularly. It is interesting to note that we’re not alone in adopting this strategy although our specific mix in each of the portfolios is unique. A recent study by mutual fund manager T. Rowe Price showed that re-balancing portfolios annually provided 20% less risk (i.e. volatility) and almost identical returns to selecting an asset allocation and never re-balancing. Harvard, the richest school in the U.S. is among a very few academic institutions whose endowments have generated stunning returns. They have done so by selecting asset allocation models which they do not alter regardless of market direction. A recent New York Times article quoted the chief strategist of Harvard’s endowment fund stating that “We have no idea which way asset classes are going to move [and] I don’t think we are smart enough to be right. I am a terrible dinner party partner. Someone will say: So what do you think of the stock market, and I will say, ‘I don’t have a clue.’“ We couldn’t have said it better ourselves. And yet, our track record using strategic asset allocation and rebalancing the portfolio allocations regularly has produced very respectable results, presented farther down the page for your review.

for selecting the appropriate model portfolio, see above

Specific Investment Products & Strategies

If you have additional interest, please click on one of the following underlined links: 1) Personal Investing; 2) Retirement Investing; 3) Investment Strategies; 4) Stocks; 5) Bonds; 6) Mutual Funds; 7) Exchange Funds; 8) Private Investments; 9) Alternative Investments; 10) 529 College Plans; 11) Coverdell Plans; 12) Fiduciary Investing; and 13) European Investing for more detailed information about each option.

Shoreline’s Competitive Edge

We are a network of independent professionals with over 150 years of combined experience in wealth management and advice. Members of this network can be used individually or collectively for a single program or a series of seminars or workshops for your company or organization.

For more information:

If you’d like more information about how diversified investment advisors can help you achieve your financial objectives through personalized wealth or retirement and risk management strategies, please contact us. We welcome the opportunity to discuss your unique needs and how we may best meet them.

This page is updated regularly so check in from time-to-time to see new articles and updates. You can click on any underlined words on each page to view a specific link or in the left margin of each page to explore a specific wealth management topic.

Charles M. Bloom, Registered Principal offers securities and advisory services through Centaurus Financial, Inc. - Member FINRA and SIPC - 775 Avenida Pequena, CA, 93111 (mailing address: 3905 State Street Suite 7173, Santa Barbara, CA, 93105) - CA Life Insurance License No. 0A52786 - Centaurus Financial, Inc. and Shoreline Wealth & Investment Management are not affiliated companies.

The information contained in this web site is neither an offer nor solicitation of any security or service.

All photos courtesy of Shoreline Summit Photography